Key Takeaways

- Inflation and economic policy have changed drastically since the 1970s, impacting how wealth is accumulated.

- Relying solely on savings may reduce purchasing power in an inflation-driven economy.

- Investing in assets that hold or grow in value, such as real estate, can help counteract inflation’s effects.

- Quantitative Easing (QE) has introduced massive cash into the economy, affecting the dollar’s value.

- Diversifying into assets that appreciate over time can offer better financial security than traditional savings.

Introduction: Why Just Saving Money Might Be a Losing Strategy

You’ve heard the classic advice: “Save your money!” But in today’s economy, focusing only on saving could actually be setting you up for financial disappointment. What if I told you that savers might be “losers” in our current economic environment? Yep, you read that right. Let’s dive into why simply saving money might be putting you at a disadvantage and what you can do instead to build real wealth.

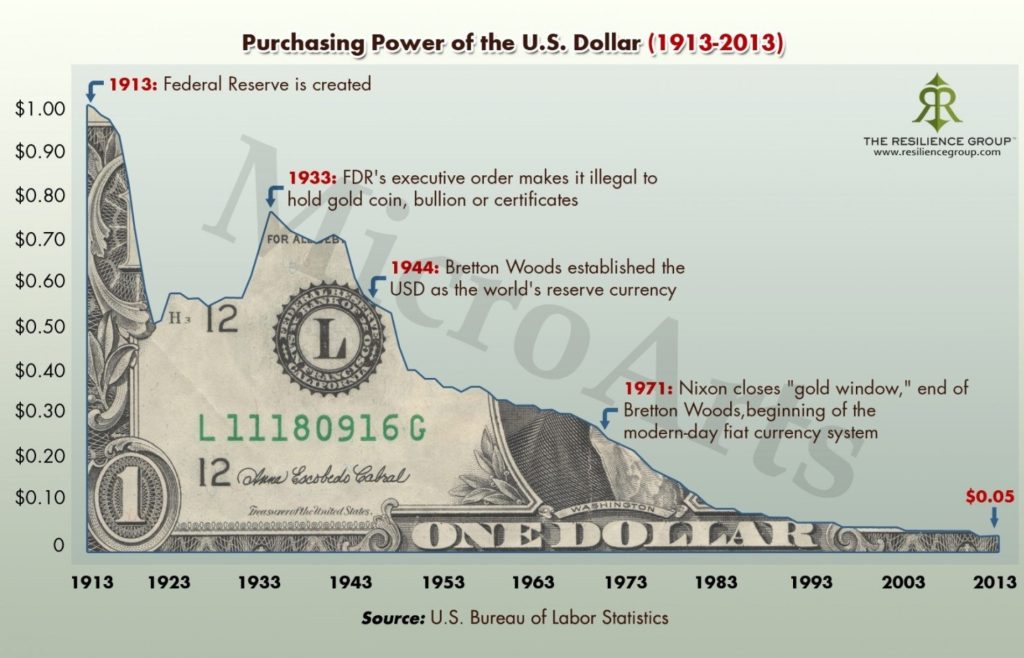

The Turning Point: 1971 and the Death of the Gold Standard

The rules of money fundamentally shifted in 1971 when President Nixon took the U.S. dollar off the gold standard. This action, known as breaking the Bretton Woods agreement, turned the U.S. dollar from a currency backed by gold into what economists call “fiat money”—meaning it’s now an instrument of debt rather than a store of intrinsic value.

Why is this important? Well, when the dollar was backed by gold, its value was stable, and saving made sense. But once the dollar became fiat money, its purchasing power started to fluctuate and, more often than not, depreciate. Since then, the dollar has lost over 85% of its purchasing power due to inflation.

The Problem with Simply Saving: Inflation Eats Away Your Cash

Imagine you save $10,000 today and stash it under your mattress. A few years from now, those savings might not buy as much as they would today. Inflation is a silent killer of purchasing power, gradually reducing what your saved dollars can get you. This is especially true as the Federal Reserve prints more money—a process known as Quantitative Easing.

Quantitative Easing (QE): The Fancy Term for “Printing Money”

To stimulate the economy, central banks sometimes resort to creating more money, a process termed Quantitative Easing. They could’ve just called it “printing money,” but that wouldn’t sound sophisticated enough, right? QE is designed to boost the economy, but the trade-off is that it increases inflation. Think of it this way: the more money there is, the less each dollar is worth. So, while your bank account balance might look impressive, its purchasing power is declining.

Breakdown of Quantitative Easing Phases:

| QE Phase | Year Initiated | Amount Created (approx.) | Main Purpose |

|---|---|---|---|

| QE1 | 2008 | $1.25 trillion | Bank bailouts post-2008 crisis |

| QE2 | 2010 | $600 billion | Lower unemployment, stabilize economy |

| QE3 | 2012 | $40 billion per month | Ongoing stimulus to spur growth |

| QE4 | 2020 | Unlimited | Pandemic response, economic stability |

The Reality Check: Saving Alone Won’t Build Wealth Anymore

So, you’ve been diligently saving, cutting back on luxuries, and living frugally. You feel like you’re doing everything right. But with inflation averaging around 3% per year and the government printing trillions, your savings lose purchasing power every year. Simply put, savers get penalized.

Here’s how inflation hits you:

- Your $1,000 savings from 2000 would only be worth around $614 in today’s purchasing power.

- By the time you hit retirement, even high-interest savings accounts might not keep pace with inflation.

Why Investing in Assets Beats Saving Alone

Saving for a rainy day is wise, but if that’s your entire strategy, you’re likely falling behind. Instead, investing in assets that either appreciate in value or generate income can be far more effective. Here are some asset classes that can help you protect and grow your wealth:

1. Real Estate

Property generally appreciates over time, particularly in growing cities or areas with demand. Additionally, rental income provides a steady stream of cash, which can be a buffer against inflation.

Example: If you bought a house for $100,000 in 2000, it could be worth around $300,000 today, depending on location and market trends.

2. Stocks and Equities

Investing in stocks can give you a stake in companies that grow over time. The S&P 500 has historically returned an average of about 10% per year. Unlike savings accounts, stocks have the potential to outpace inflation.

| Year | Average S&P 500 Return | Inflation Rate |

|---|---|---|

| 1990 | 6.57% | 5.4% |

| 2000 | -10.1% | 3.4% |

| 2010 | 15.1% | 1.6% |

| 2020 | 18.4% | 1.2% |

3. Precious Metals (Gold, Silver)

Gold and silver are often seen as “safe haven” assets. They don’t produce income, but they retain value over long periods, making them useful as a hedge against inflation.

Example: In 1971, an ounce of gold was around $35. Today, it’s priced at over $1,800 per ounce.

4. Collectibles

Investing in rare items, like art, vintage cars, and antiques, can also yield significant returns. A prime example is the 1962 Ferrari 250 GTO, which once sold for $34.65 million. While collectibles are more niche, they can be lucrative if you know what you’re doing.

How to Start Building Wealth Beyond Savings

Let’s say you’re ready to get into assets but don’t know where to start. Here are some easy, beginner-friendly steps to start building wealth beyond just saving:

- Start Small with Stock Investments: You can begin by investing a small amount in index funds, which track a particular market index. With platforms like Robinhood or E*TRADE, you can get started with as little as $100.

- Invest in Real Estate Crowdfunding: Platforms like Fundrise or Roofstock let you invest in real estate with a few hundred dollars. These options give you exposure to real estate markets without needing to buy an entire property.

- Diversify into Precious Metals: While you don’t need to buy a gold bar, you can purchase small amounts of gold or silver through online platforms.

- Consider Cryptocurrencies Cautiously: Crypto assets like Bitcoin are volatile, but some view them as a digital hedge against inflation. Start with a minimal investment if you’re interested but don’t rely on crypto alone.

Real-Life Example: Investing vs. Saving for 20 Years

To illustrate the impact of investing vs. saving, let’s consider two hypothetical individuals:

| Person | Action Taken | Initial Amount | Annual Return | Value After 20 Years |

|---|---|---|---|---|

| Saver | Saved in a High-Yield Account | $10,000 | 1% | $12,202 |

| Investor | Invested in an S&P 500 ETF | $10,000 | 8% | $46,610 |

As you can see, the investor’s money grows significantly more than the saver’s over the same period, even with modest annual returns.

Conclusion: Don’t Just Save—Invest to Protect and Grow Your Wealth

In today’s economy, simply saving money might not be enough to secure a financially stable future. Inflation and economic policies like QE mean that relying on a traditional savings account alone could cause your purchasing power to shrink. Instead, consider diversifying your savings into appreciating assets, whether it’s real estate, stocks, or precious metals.

So, next time someone tells you to “just save your money,” you can confidently tell them you’re investing to protect your future! Remember, the best way to ensure financial freedom is by making your money work for you instead of sitting idle in a savings account.